7 Easy Facts About Chapter 7 Vs Chapter 13 Bankruptcy Explained

7 Easy Facts About Chapter 7 Vs Chapter 13 Bankruptcy Explained

Blog Article

The Single Strategy To Use For Which Type Of Bankruptcy Should You File

Table of ContentsIndicators on Bankruptcy Attorney Tulsa You Should KnowNot known Facts About Tulsa Bankruptcy Filing AssistanceSome Known Incorrect Statements About Chapter 7 - Bankruptcy Basics The Of Which Type Of Bankruptcy Should You FileSome Ideas on Experienced Bankruptcy Lawyer Tulsa You Should KnowThe Ultimate Guide To Experienced Bankruptcy Lawyer Tulsa

People must use Chapter 11 when their debts go beyond Chapter 13 debt limitations. It seldom makes good sense in various other instances but has more choices for lien removing and cramdowns on unsafe sections of secured finances. Phase 12 personal bankruptcy is made for farmers and fishermen. Phase 12 settlement plans can be a lot more flexible in Chapter 13.The means test takes a look at your average regular monthly income for the six months preceding your filing day and compares it versus the mean earnings for a similar household in your state. If your income is listed below the state typical, you instantly pass and do not have to finish the whole form.

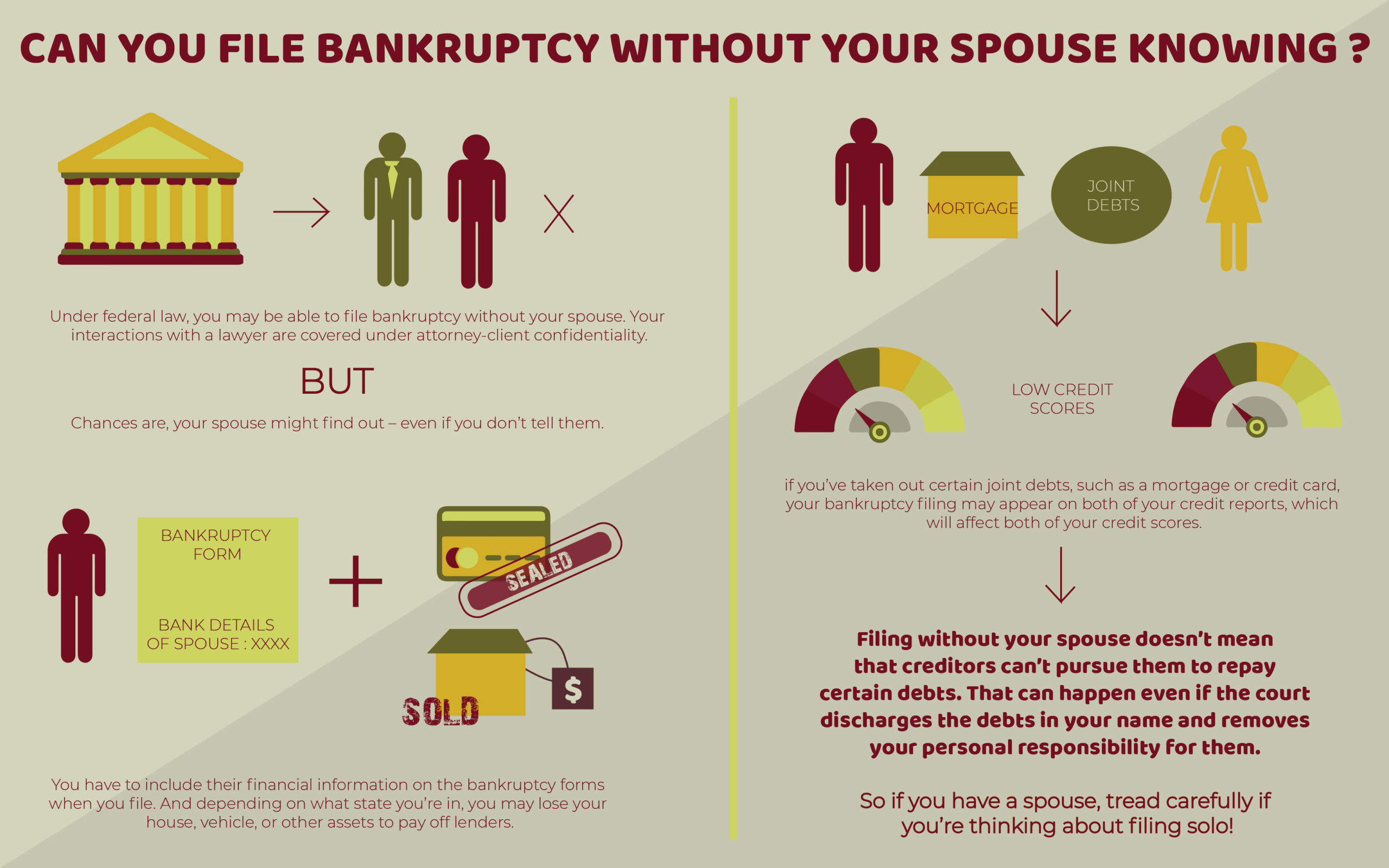

The financial obligation restrictions are listed in the graph above, and current quantities can be validated on the United State Judiciaries Phase 13 Bankruptcy Essential webpage. Find out more regarding The Means Examination in Phase 7 Insolvency and Financial Debt Boundaries for Chapter 13 Insolvency. If you are wed, you can declare insolvency jointly with your partner or individually.

Filing insolvency can help a person by throwing out financial debt or making a plan to settle financial obligations. An insolvency situation typically begins when the borrower files a petition with the personal bankruptcy court. There are various kinds of personal bankruptcies, which are generally referred to by their phase in the United state Insolvency Code.

If you are encountering monetary difficulties in your individual life or in your company, opportunities are the concept of filing personal bankruptcy has crossed your mind. If it has, it likewise makes feeling that you have a lot of bankruptcy inquiries that require solutions. Many individuals really can not answer the question "what is personal bankruptcy" in anything except general terms.

If you are encountering monetary difficulties in your individual life or in your company, opportunities are the concept of filing personal bankruptcy has crossed your mind. If it has, it likewise makes feeling that you have a lot of bankruptcy inquiries that require solutions. Many individuals really can not answer the question "what is personal bankruptcy" in anything except general terms.Many individuals do not realize that there are several sorts of bankruptcy, such as Phase 7, Chapter 11 and Phase 13. Each has its advantages and challenges, so understanding which is the most effective option for your existing circumstance as well as your future recuperation can make all the distinction in your life.

Chapter 7 Vs Chapter 13 Bankruptcy - The Facts

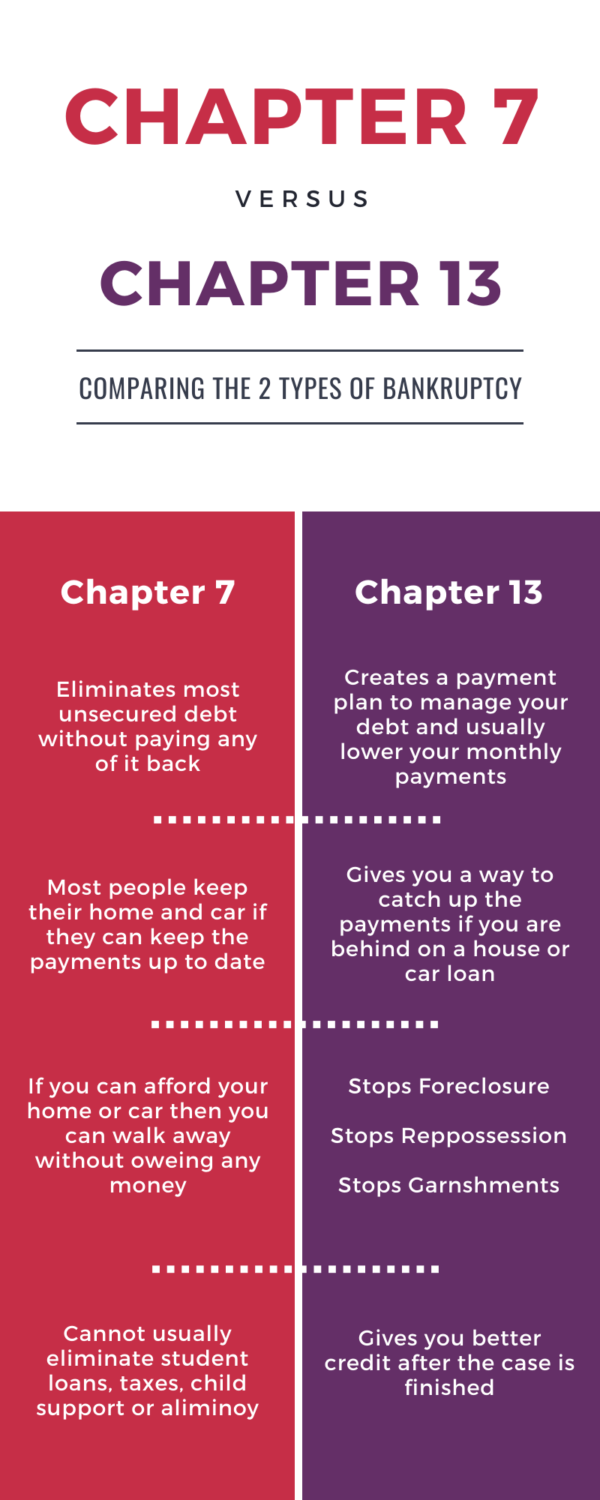

Phase 7 is described the liquidation bankruptcy chapter. In a phase 7 insolvency you can eliminate, clean out or discharge most kinds of debt.

Numerous Phase 7 filers do not have a lot in the means of properties. Others have residences that do not have much equity or are in significant requirement of repair work.

The quantity paid and the duration of the strategy depends on the borrower's property, typical revenue and expenditures. Financial institutions are not permitted to pursue or maintain any kind of collection activities or legal actions throughout the situation. If successful, these creditors will over here certainly be erased or discharged. A Phase 13 personal bankruptcy is really powerful since it gives a mechanism for borrowers to avoid repossessions and constable sales and quit foreclosures and energy shutoffs while catching up on their secured financial debt.

See This Report about Tulsa Debt Relief Attorney

A Phase 13 situation may be helpful because the borrower is allowed to get captured up on home loans or auto loan without the risk of foreclosure or foreclosure and is allowed to maintain both excluded and nonexempt residential or commercial property. The borrower's strategy is a file detailing to the personal bankruptcy court exactly how the debtor suggests to pay current expenditures while repaying all the old financial debt balances.

It provides the borrower the opportunity to either offer the home or end up being caught up on home loan settlements that have actually dropped behind. An individual submitting a Phase 13 can recommend a 60-month plan to treat or become current on home loan settlements. For circumstances, my link if you dropped behind on $60,000 well worth of mortgage repayments, you can propose a plan of $1,000 a month for 60 months to bring those home loan payments current.

It provides the borrower the opportunity to either offer the home or end up being caught up on home loan settlements that have actually dropped behind. An individual submitting a Phase 13 can recommend a 60-month plan to treat or become current on home loan settlements. For circumstances, my link if you dropped behind on $60,000 well worth of mortgage repayments, you can propose a plan of $1,000 a month for 60 months to bring those home loan payments current.The 6-Second Trick For Best Bankruptcy Attorney Tulsa

Often it is much better to avoid bankruptcy and clear up with financial institutions out of court. New Jersey also has an alternative to personal bankruptcy for services called an Project for the Benefit of Creditors and our law office will look at this option if it fits as a potential strategy for your company.

We have produced a device that assists you select what phase your data is more than likely to be filed under. Click here to utilize ScuraSmart and discover a feasible remedy for your debt. Lots of people do not recognize that there are several types of personal bankruptcy, such as Phase 7, Phase 11 and Chapter 13.

Right here at Scura, Wigfield, Heyer, Stevens & Cammarota, LLP we manage all kinds of bankruptcy cases, so we have the ability to address your personal bankruptcy questions and assist you make the very best choice for your situation. Right here is a quick consider the debt relief alternatives offered:.

The 6-Second Trick For Tulsa Bankruptcy Attorney

You can only submit for insolvency Prior to filing for Chapter 7, at least one of these need to be real: You have a whole lot of financial debt revenue and/or possessions a financial institution can take. You have a great deal of financial debt close to the homestead exemption amount of in your home.

The homestead exception amount is the better of (a) $125,000; or (b) the area mean list price of a single-family home in the preceding calendar year. is the amount of money you would certainly keep after you offered your home and paid off the mortgage and other liens. You can find the.

Report this page